时间:2024-04-07|浏览:255

本周,美联储官员意外释放鹰派信号,美国经济数据打压降息预期,中东紧张局势升级。原油价格连续第四周上涨,布伦特原油数月来首次收于每桶90美元上方。现货黄金继续上涨,突破2300美元/盎司关口,连续第三周上涨。白银也实现周涨幅,接近近三年来的最高水平。无论市场认为美联储会降息还是加大降息力度,黄金似乎并不在意,强劲的美国非农数据也被忽视。中东和乌克兰紧张局势升级等问题增加了黄金和原油的吸引力。

美股、债市和汇市二季度首周均遭遇“糟糕开局”,交易员进行鹰派重新定价。道琼斯指数下跌2.27%,创2023年3月10日当周(硅谷银行倒闭当周)以来最大单周跌幅;标准普尔指数下跌0.95%,纳斯达克指数和纳斯达克100指数均下跌0.8%。 10年期美债收益率本周上涨约20个基点,对利率前景较为敏感的2年期美债收益率本周上涨约13个基点,连续两周上涨。美元指数本周下跌近0.2%,在连续三周上涨后回落。不过,值得注意的是,令人兴奋的非农报告发布后,美股本周收涨,表明美国经济将继续为美国企业提供动力。尽管这意味着利率可能维持在高位,但华尔街决定看事情积极的一面——经济表现良好。

未来一周,美国将公布CPI、PPI等最新数据,这或许是美联储6月是否降息的“更大试金石”。

以下是新一周市场关注的重点(均为北京时间):

央行消息:地缘政治避险情绪击败美联储言论,黄金净多头一周飙升13%

美联储:降息预期再次混乱,会议纪要将提供更多线索

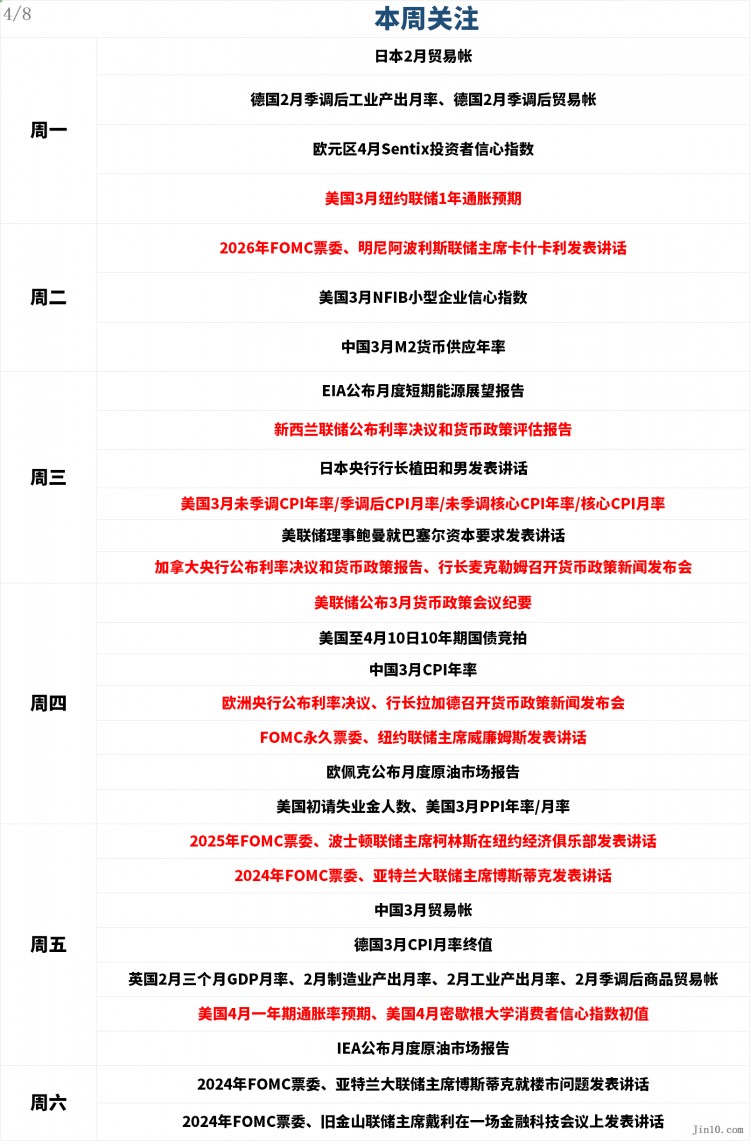

周二07:00,2026年FOMC投票委员、明尼阿波利斯联储主席卡什卡里发表讲话

周三 20:45,美联储理事鲍曼将就巴塞尔资本要求发表讲话

周四凌晨2:00,美联储将公布3月份货币政策会议纪要。

周四20点45分,FOMC常任投票委员、纽约联储主席威廉姆斯发表讲话

At 00:00 on Friday, Collins, 2025 FOMC voting member and President of the Boston Fed, delivered a speech at the New York Economic Club.

At 01:30 on Friday, Bostic, the 2024 FOMC voting member and President of the Atlanta Fed, will deliver a speech

At 02:30 on Saturday, 2024 FOMC voting member and Atlanta Fed President Bostic will speak on the housing market

At 03:30 on Saturday, Daly, the 2024 FOMC voting member and president of the San Francisco Fed, spoke at a fintech conference.

Ten of the Fed's 12 rate-setting voters have made at least 20 public appearances in the past two weeks, giving market watchers plenty to comment on. However, expectations for a Fed rate cut are back in disarray. After the March nonfarm payrolls report, traders no longer fully expect the Fed to cut rates before September. Swap contracts put the odds of a June rate cut at around 52%, while the odds for July have fallen to below 100%. Investors are now hoping that the minutes of the Fed's March meeting, due out next week, and speeches from several top Fed officials will provide more clarity.

If consumer spending and corporate profits outweigh when and how often the Federal Reserve will cut interest rates, stocks could rise, according to stock investors. The fact that the labor market is so strong suggests companies and the economy are adjusting to higher interest rates.

Gold investors have also made their own judgments. Compared with the volatile US economic data and speeches of Federal Reserve officials, they are more concerned about the safe-haven demand brought about by geopolitical risks in the Middle East. Hedge funds and money managers have increased their bullish bets on gold. Data released by the U.S. Commodity Futures Trading Commission (CFTC) on Friday showed that their net long positions in U.S. gold futures and options soared 13% in the week ending April 2, reaching the highest level since 2020.

Activity in the gold options market has been unusually high compared to markets such as stocks and bonds, meaning that current interest is focused on gold. While the gold market may not be going completely "crazy" and technically the market may be overbought and feel at risk of a sharp drop, analysts remain bullish. "It's hard to say where the price top is as there aren't any resistance 'signposts' on the chart," said Edward Meir, an analyst at Marex.

Other central banks: The three major central banks are about to make interest rate decisions, and the yen is in a dilemma

At 10:00 on Wednesday, the Reserve Bank of New Zealand will announce its interest rate decision and monetary policy assessment report.

At 14:00 on Wednesday, Bank of Japan Governor Kazuo Ueda will deliver a speech

At 21:45 on Wednesday, the Bank of Canada announced its interest rate decision and monetary policy report; at 23:00, Bank of Canada Governor Macklem held a monetary policy press conference

At 20:15 on Thursday, the ECB announced its interest rate decision; at 20:45, ECB President Lagarde held a monetary policy press conference

According to a Reuters survey, all 29 economists believe that the Reserve Bank of New Zealand will keep the benchmark interest rate unchanged at 5.50% on April 10. The median forecast shows that the Reserve Bank of New Zealand will keep the benchmark interest rate unchanged at 5.50% in the second quarter and will cut it by more than 25 basis points in the third quarter.

TD Securities believes that the weak employment data will keep the Bank of Canada cautious. Tu Nguyen, an economist at RSM Canada, a Canadian tax and accounting firm, said Canada's weak employment report in March further proves that the Bank of Canada will cut interest rates in June at the latest. BMO Capital Markets also said that the contradictory employment data signals will not hinder the dovish tendency of the Bank of Canada, and the central bank may be ready to cut interest rates in June. According to a Reuters poll, the Canadian dollar is expected to rise to 1.34 against the US dollar in three months, an increase of 0.9%, in line with the forecast in March. The Canadian dollar will rise to 1.31 against the US dollar in one year, an increase of about 3.2%, and the forecast in March is 1.30.

As for the ECB, no rate cut is expected next week, and the focus remains on whether there will be a rate cut in June. Eurozone inflation slowed more than expected in March, which consolidates the prospect of a rate cut by the ECB in June, with the base case being a 100 basis point cut this year. A dovish ECB stance could highlight policy divergence with the Fed and lead to capital outflows from the euro to the dollar. In this case, broad dollar strength could make it difficult for gold to gain momentum.

Kazuo Ueda will speak again next week. Verbal intervention by Japanese authorities this week has been effective in slowing the pace of further weakness in the yen, which has also been boosted by risk aversion, but the yen remains at the mercy of the U.S. economy. Bank of Japan Governor Kazuo Ueda will speak on the same day as the U.S. CPI is released next week, and on the same day that Japanese Prime Minister Fumio Kishida will meet with U.S. President Biden in Washington. While the timing may be awkward for Japanese intervention, the risk is that the yen could continue to depreciate if it falls below 152 and authorities fail to match words with actions. Japan's leaders have pledged to take appropriate action against excessive volatility. Many economists warn that the Bank of Japan may need to make another rate hike sooner than expected.

Important data: CPI is coming, the US dollar is easy to rise but difficult to fall

Monday 23:00, US New York Fed 1-year inflation forecast for March

Tuesday 18:00, US March NFIB Small Business Confidence Index

On Wednesday, EIA released its monthly Short-Term Energy Outlook report

At 20:30 on Wednesday, the US March unadjusted CPI annual rate/seasonally adjusted CPI monthly rate/unadjusted core CPI annual rate/core CPI monthly rate

At 22:00 on Wednesday, the monthly rate of wholesale sales in the United States in February

Thursday 01:00, US 10-year Treasury auction until April 10 - winning interest rate/bid multiple

Thursday 09:30, China's March CPI annual rate

At 20:30 on Thursday, the annual rate/monthly rate of PPI in March in the United States

On Thursday, OPEC released its monthly crude oil market report.

At 14:00 on Friday, the final monthly rate of German CPI in March; the monthly rate of UK GDP in February, the monthly rate of manufacturing output in February, the monthly rate of industrial output in February, and the seasonally adjusted commodity trade account in February

At 16:00 on Friday, the IEA released its monthly crude oil market report

At 22:00 on Friday, the U.S. one-year inflation rate forecast for April and the preliminary value of the University of Michigan Consumer Confidence Index for April

Despite the strong non-farm report released on Friday, the average hourly wage rate fell to 4.1% on an annual basis, the lowest level since June 2021. Some analysts therefore believe that this is still a report showing cooling inflation, and the non-farm data depicts a "Goldilocks" scenario, and the Fed can still maintain its expectation of three rate cuts. Next Wednesday's US CPI report is crucial to the Fed's interest rate expectations and the trend of the US dollar. CPI and core CPI are expected to rise by 0.3% month-on-month.

Given the solid employment data and ongoing inflation concerns, the US dollar index is likely to remain strong in the short term. The market currently tends to be bullish on the dollar outlook, reflecting confidence in the underlying strength of the US economy. 105 is likely to be an important near-term peak for the US dollar index, but US data would have to be soft to pull it back to 103 again.

If the monthly core CPI rises faster than expected, it could immediately boost the dollar and trigger a downside correction in gold. On the other hand, a reading of 0.2% or lower could reignite expectations for a rate cut in June and hurt the dollar.

Also not to be overlooked is Thursday's release of the US Producer Price Index (PPI) for March. In the past, market participants have paid little attention to producer inflation data. However, recent PPI releases have triggered huge reactions. PPI rose 0.6% in February. Another strong increase in March data could affect expectations that consumer inflation will remain stable and support the dollar.

Speculative long positions in the euro have been cut in half from their December highs, and there seems to be a lack of catalysts to push the next move lower. The eurozone economy also seems to be stabilizing, and natural gas prices are also falling. On the contrary, long positions in the pound are at a multi-year high, and signs of deflation in the second quarter may increase expectations of a rate cut by the Bank of England, which will bring room for the euro to rise against the pound.

Important events: The situation in the Middle East has changed suddenly, beware of the driving force behind the surge in oil prices

Heightened tensions in the Middle East have triggered a dramatic repricing of geopolitical risks. Concerns about a wider regional conflict are growing, and Israel is stepping up preparations for a retaliatory attack from Iran. "The market now knows that Iran is likely to retaliate in some way, but it doesn't know when, where or what, which creates a lot of uneasiness and tension," said Bjarne Schieldrop, chief commodities analyst at SEB AB.

CNN quoted a senior US government official as saying that the United States is on "high alert" for the attack on the Iranian embassy building in Syria and is actively preparing to respond to a "major" attack by Iran against Israel or US assets in the region, which may be launched as early as next week, but as of the 5th, they are still unclear when and how Iran plans to retaliate. According to CBS, US officials said that intelligence obtained by the US shows that Iran may use a large number of "Shahed" drones and cruise missiles in retaliatory attacks, and may attack Israeli diplomatic facilities equivalent to the Iranian embassy, probably between now and the end of Ramadan next week.

Heightened tensions are also spurring activity in the oil options market, where volatility is surging and call options are trading at a rare premium over put options. Oil prices are likely to remain at their current highs as geopolitical risk factors increase, but the next big move could come if Israel attacks Iranian energy facilities, said Greg Sharenow, head of commodities portfolio management at Pacific Investment Management Co.

"I think the way that will really affect the broader oil market balance is if Israel seeks to attack Iran's energy infrastructure," Sharenow said in an interview, adding that this would be a way to weaken Iran by reducing its oil revenues. Sharenow warned that such an approach would draw a lot of opposition from other world leaders but was more risky, especially because Ukraine has been targeting Russian refineries in the Russo-Ukrainian conflict.

He also said that at this point, any additional U.S. oil release from the Strategic Petroleum Reserve would likely result in significant losses in physical supply, especially because it might make Saudi Arabia reluctant to ease current supply restrictions.

Company financial report:

The first-quarter earnings season for U.S. stocks will officially kick off next week, with JPMorgan Chase, Wells Fargo and Citigroup all set to announce their results on Friday.

“Earnings season will likely show a bifurcated market, with many companies thriving but an increasing number struggling,” said Yung-Yu Ma of BMO Wealth Management. “To some extent, this reflects the overall economy, with lower socioeconomic groups facing greater pressure, but the bifurcation is also a result of rising interest rates and other changes in the economy.”

Bank of America strategists cited EPFR Global data, saying that investors poured $7.1 billion into U.S. stocks in the week ending Wednesday. Annualized capital flows into U.S. stocks reached $310 billion, the second highest ever. Annualized capital flows into technology stocks reached $73 billion, a record high.

Market Holiday Arrangement

On Wednesday (April 10), the Seoul Stock Exchange in South Korea was closed for one day due to the South Korean presidential election.

Article forwarded from: Jinshi Data

用戶喜愛的交易所

已有账号登陆后会弹出下载